21 / 158

21 / 158

page

19

FIMA CORPORATION BERHAD

(21185-P) |

Annual Report

2016

MANAGEMENT DISCUSSION

AND ANALYSIS

(contd.)

PLANTATION

BUSINESS OPERATION REVIEW

The Plantation Division recorded RM102.6 million revenue, a decrease of RM4.5 million compared to last year.

PBT registered was RM 21.4 million, a decrease of 38.0% year-on-year. The decline in revenue and PBT was

primarily attributable to decrease in CPO average CIF selling price realised of RM2,064 per metric tonne (“mt”)

compared to RM2,207 per mt in the previous year. The CPO price was also negatively impacted by an export levy

of USD50 per mt imposed by the Indonesian government effective 16 July 2015.

For the period under review, the Group’s Indonesian subsidiary, PT Nunukan Jaya Lestari harvested 149,060 mt

(FY2015: 149,701 mt) fresh fruit bunches (“FFB”), 0.4% decrease year-on-year. The average yield per mature

hectare had marginally decreased to 23.17 mt/ha (FY2015: 23.14 mt/ha), mainly due to the prolonged dry weather

experienced during the year. Purchase of FFB from third parties decreased to 53,198 mt from 60,677 mt last year.

Production of CPO and crude palm kernel oil during the year totalled 45,387 mt (FY2015: 47,649 mt) and 3,363 mt

(FY2015: 1,191 mt) respectively. The average oil extraction rate of 22.42% was marginally lower than last year’s

rate of 22.71%.

During FY2016, the Division spent RM10.6 million on CAPEX, largely towards plantation development works,

construction and refurbishment of workers quarters as well as estate equipment.

Indonesia

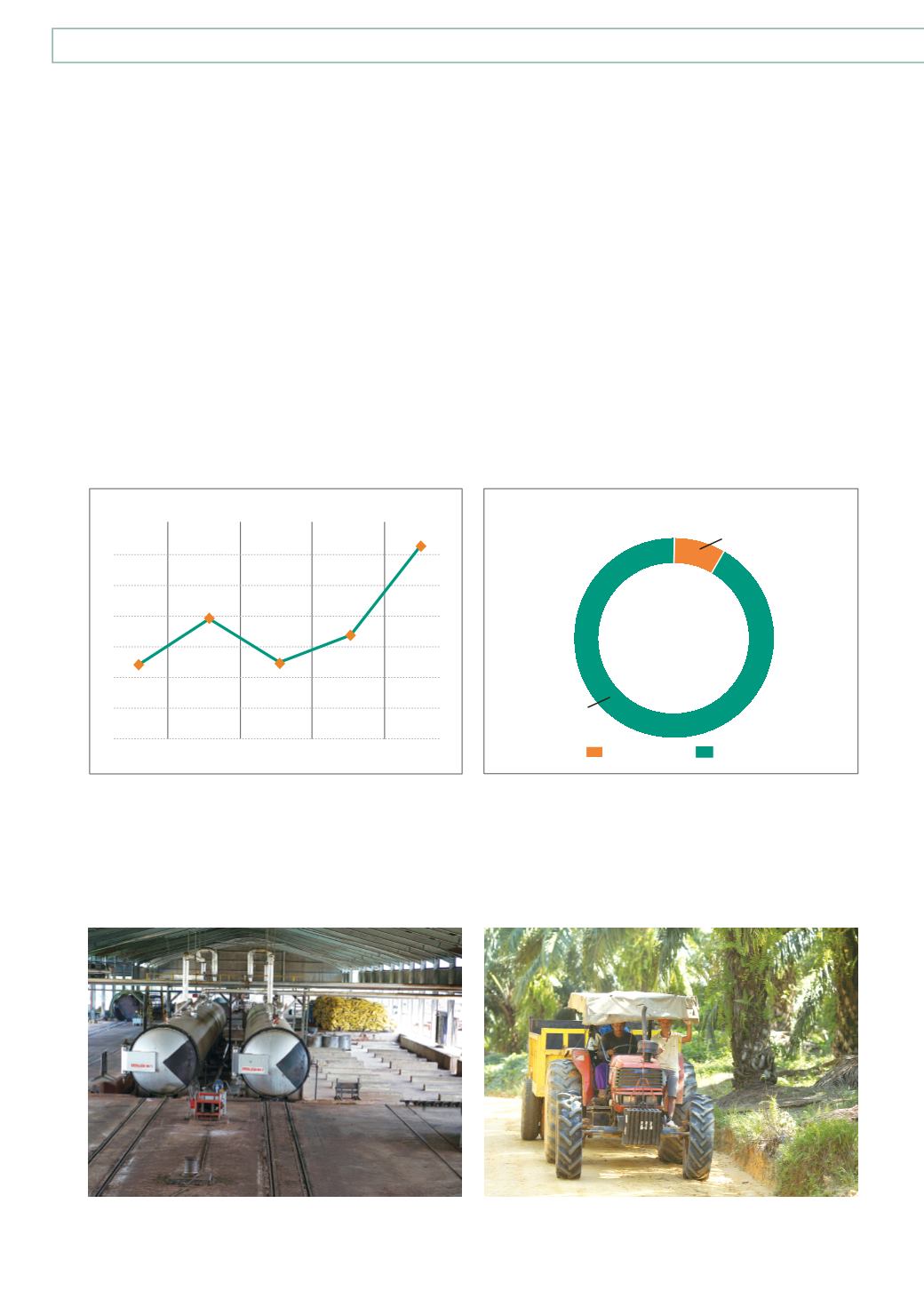

PLANTED AREA (HA)

Peninsula

489.09

6,432.99

AVERAGE CPO PRICE REALISED

2016

2015

2014

2013

2012

2,064

2,430

2,155

2,068

2,207