46 / 204

46 / 204

Immature palms make

up 1,560 ha of the

Group’s total planted

area, which means

the Group’s crops

are projected to rise

strongly in the

coming years.

Group FFB

Harvested

(MT)

166,080

FYE2019

FYE2018

175,774

Meanwhile, PBT stood at RM23.80

million (before the writeback

of impairment losses which is

discussed hereinbelow), which

was 40.9% lower than the PBT

of RM40.28 million achieved last

year. Our estates in Malaysia which

are still in the process of land

development or palm planting

registered a higher total pretax loss

of RM4.5 million compared to RM2.5

million pretax loss recorded last

year following to the acquisition of

Ladang Bunga Tanjong Sdn. Bhd.

which was completed in February

2018.

The division had in Q2 FYE2019

reversed a previously recorded

impairment on property, plant

and equipment in the Group’s

Indonesian subsidiary, PT Nunukan

Jaya Lestari (“PTNJL”) as a

consequence of the Mahkamah

Agung’s decision that the Ministerial

Order revoking PTNJL’s HGU

be annulled. The reversal of the

impairment has a positive effect

of RM23.63 million whereupon the

division’s PBT for FYE2019 would be

RM47.43 million with the inclusion

of the writeback.

FFB produced by PTNJL decreased

6.1% to 164,770 MT (FYE2018:

175,425 MT). A lower average

yield per hectare of 25.98 MT was

recorded compared to 27.53 MT

last year. FFB purchased from third

parties also decreased to 49,902

MT from 60,460 MT in prior year.

Note that FFB production was back

to normal following to the bumper

crops recorded last year which is

due to post recovery of El-Nino.

CPO and CPKO production during

the year under review were 47,966

MT and 4,434 MT respectively

(FYE2018: 51,887 MT and 4,013

MT respectively) in line with the

decline in FFB production and

lower third-party crop. Average

CPKO price was RM3,015 per MT,

compared with RM4,431 per MT in

prior year. Meanwhile, the Group’s

oil extraction rate (“OER”) average

of 22.34% was slightly higher

compared to 22.09% OER recorded

last year.

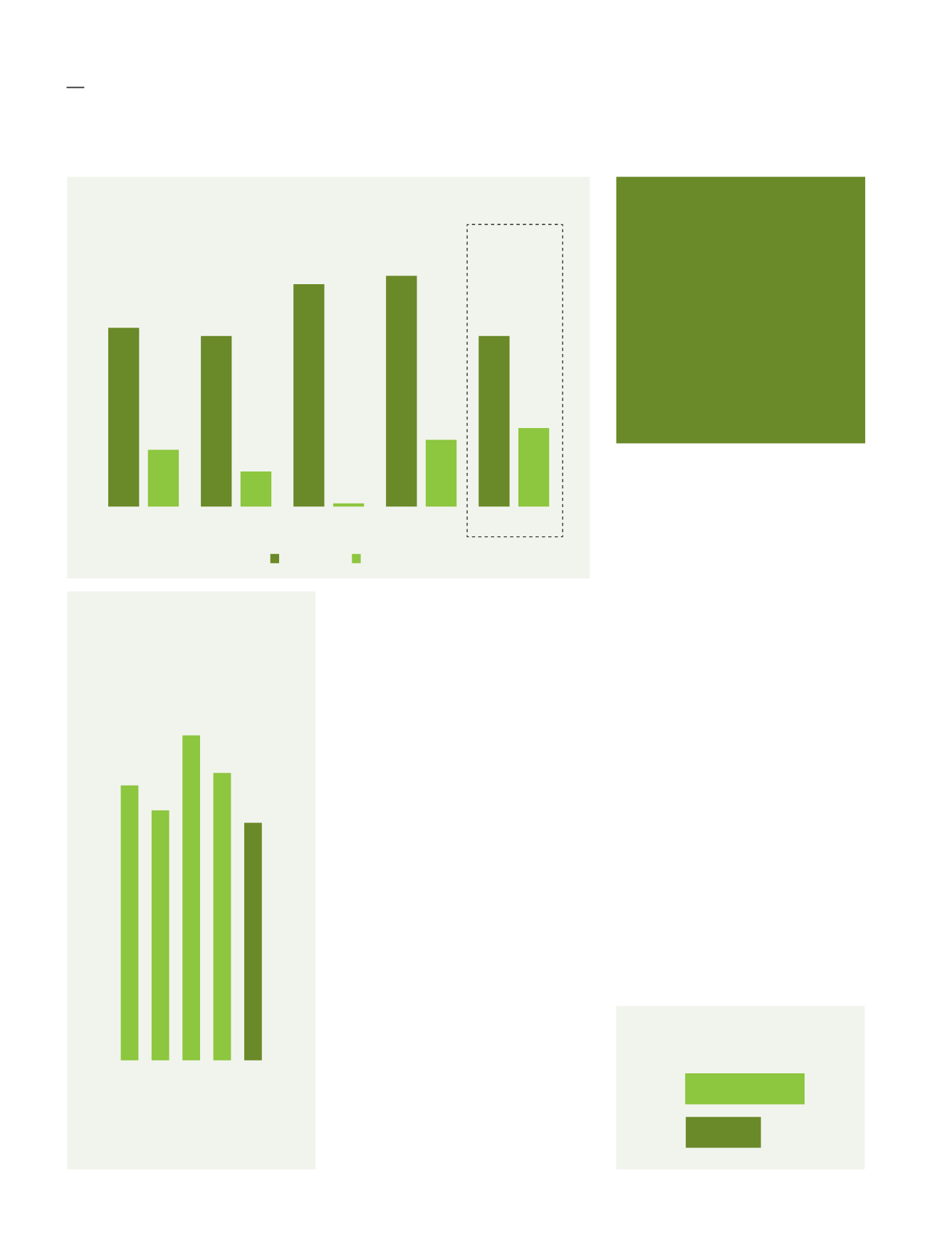

5-Year Revenue & PBT

Performance

(RM Million)

FYE2018

FYE2016

FYE2015

FYE2019

FYE2017

47.43

+17.8%

102.84

-25.5%

40.28

(0.55)

138.10

133.21

21.35

102.61

34.42

107.12

Revenue

PBT

Average CPO

Price Realised

(RM/MT)

FYE2015

2,207

2,064

2,625

2,342

1,921

FYE2016

FYE2017

FYE2018

FYE2019

Fima CORPORATION Berhad

(21185-P)

Annual Report 2019

42