36 / 204

36 / 204

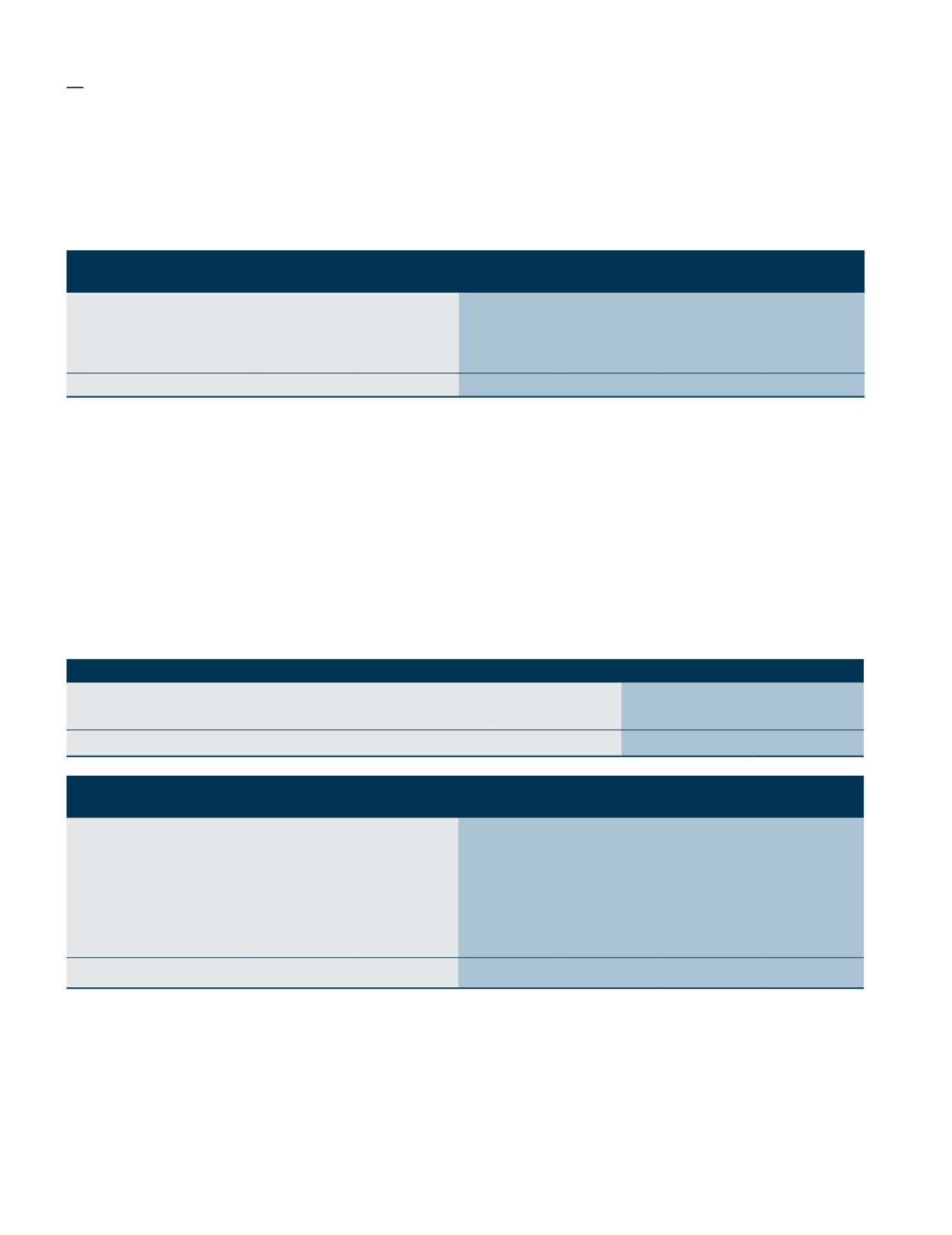

Segmental Revenue Analysis

Breakdown of revenue by division:

FYE2018

RM Million

Contribution

%

FYE2019

RM Million

Contribution

%

Variance

RM Million

Variance

%

Manufacturing

140.78

49.5

134.78

55.1

(6.00)

(4.3)

Plantation

138.10

48.5

102.84

42.0

(35.26)

(25.5)

Property Management

5.77

2.0

7.10

2.9

1.33

23.1

Group Results

284.65

100.0

244.72

100.0

(39.93)

(14.0)

The Group recorded revenue of RM244.72 million (FYE2018: RM284.65 million) during the financial year,

representing a decrease of 14.0% compared to the previous year, reflecting the lower contributions from our

Manufacturing and Plantation divisions. Meanwhile, Property Management’s revenue improved by RM1.33 million

year-on-year (“y-o-y”) due to positive contributions from the division’s engineering consultation services unit.

Manufacturing division revenue declined by 4.3% to RM134.78 million, impacted by the expiration of the contract to

supply certain travel document products.

The drop in Plantation’s revenue was largely due to lower commodity prices coupled with a reduction in fresh fruit

bunches (“FFB”) produced during the financial year. Our average CIF Crude Palm Oil (“CPO”) (net of duty) selling

price in FYE2019 declined significantly by 18.0% to RM1,921 per MT (FYE2018: RM2,342 per MT). The average Crude

Palm Kernel Oil (“CPKO”) price achieved was also lower y-o-y at RM3,015 per MT (FYE2019: RM4,431 per MT).

FYE2018

FYE2019 Change %

CPO

RM2,342 per MT RM1,921 per MT

(18.0)

CPKO

RM4,431 per MT RM3,015 per MT

(32.0)

FFB Production

175,774 MT

166,080 MT

(5.84)

FYE2018

RM Million

Contribution

%

FYE2019

RM Million

Contribution

%

Variance

RM Million

Variance

%

Manufacturing

22.81

37.4

30.56

38.5

7.75

34.0

Plantation

40.28

66.1

47.43

59.7

7.15

17.8

Property Management

1.61

2.6

1.45

1.8

(0.16)

(9.9)

Share of Results of

Associate

1.70

2.8

3.73

4.7

2.04

120.0

Others

(5.43)

(8.9)

(3.70)

(4.7)

1.73

(31.9)

Group Results

60.97

100.0

79.48

100.0

18.51

30.4

The Group’s PBT in FYE2019 was RM79.48 million compared to RM60.97 million recorded in the prior year. The

increase in the PBT by 30.4% y-o-y was mainly attributed to the reversal of previous impairment on PPE in Q2

FYE2019 of RM23.63 million. Without the write back of the impairment, the Group PBT would be RM55.85 million,

8.40% lower from previous year.

Meanwhile, Manufacturing division’s recorded better PBT against last year was primarily due to higher write back

of inventories and reversal of certain provisions as well as lower direct costs and depreciation.

Fima CORPORATION Berhad

(21185-P)

Annual Report 2019

32