27 / 174

27 / 174

performance

Annual Report 2017

25

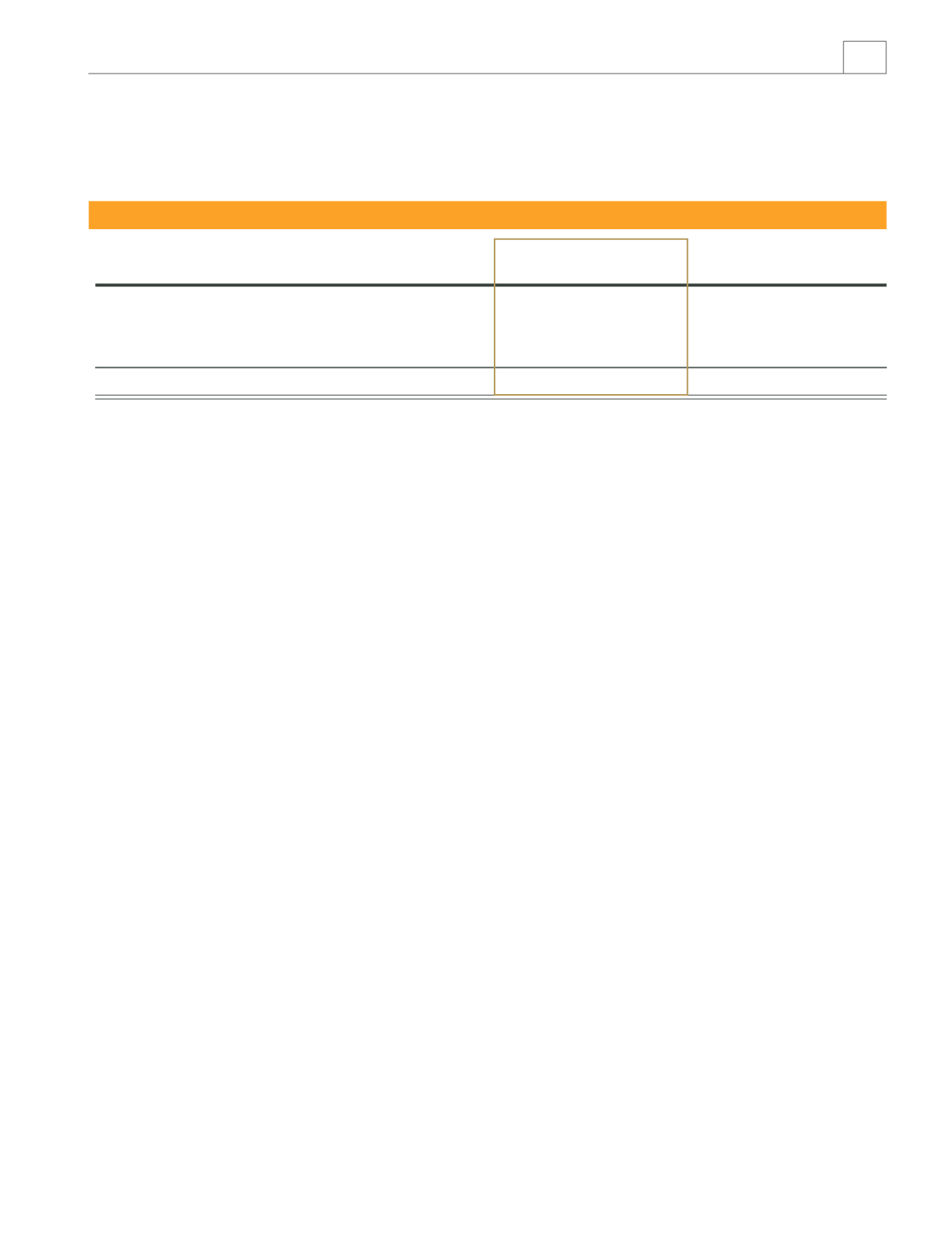

SEGMENTAL profit before tax (“pbt”)

2017 Contribution

2016 Contribution

RM’million

% RM’million

%

Manufacturing

59.6

97.2

54.0

69.9

Plantation

(0.7)

(1.1)

21.3

27.6

Share of results of associate

2.7

4.4

1.6

2.0

Property Management

(0.3)

(0.5)

0.4

0.5

Group results

61.3

100.0

77.3

100.0

The Group’s PBT

decreased by 20.7% to RM61.3 million

from RM77.3 million recorded in the previous financial year. The

decrease is solely due to impairment losses on property, plant and

equipment and biological assets in a subsidiary, PT Nunukan Jaya

Lestari (“PTNJL”) mitigated by improved CPO and CPKO prices

coupled with lower cost of sales during the year. Our plantation

estates in Kelantan and Terengganu which are undergoing land

development and palm planting recorded RM2.5 million pretax

loss during the financial year.

Financial Resources and Liquidity

The group generated a

Net Cash

of RM196.3 million from its

operating activities for FYE2016/17 against RM63.9 million in the

previous financial year. This increase reflects cash proceeds from

the trade debtors.

Gross Profit

for the Group had improved by 21.1% to RM142.5

million from RM117.7 in FYE2015/16. The Group’s improved

gross profit was mainly due to a reduction in direct costs.

The Group registered a 20.7% shortfall on

EBIT

against the

same period last year, recording RM61.3 million for FYE2016/17.

This was mainly due to RM29.4 million net impairment losses on

property, plant and equipment and biological assets of PTNJL

subsequent to the State Administrative Court’s decision on

13 June 2017 to dismiss PTNJL’s application to annul the

Ministerial Order. On 21 June 2017, PTNJL had filed an application

to the Court of Appeal to appeal against the decision of the State

Administrative Court.

The Group’s

Cash and Bank Balance

, which were primarily

denominated in Ringgit and Indonesian Rupiah, stood at

RM336.3 million as at 31 March 2017 compared to RM177.6

million last year. By our current cash position and the ability to

generate cash from operations, we believe we have the sufficient

capital resources and liquidity to meet our commitments, support

operations, and growth strategies, finance capital expenditures,

and fund declared dividends.

Shareholders’ Equity

as at 31 March 2017 stood at RM586.8

million, an increase of RM4.4 million or 0.8% over the previous

financial year.

With the decrease in PAT, the Group recorded

ROAE

of 6.0%

for FYE2016/17 as compared to 9.6% recorded in the previous

financial year.

ROACE

fell to 10.1% during the year compared to 13.0% in

FYE2015/16 due to lower EBIT recorded.

The

Share of Results of Associates

in FYE2016/17 increased

by 68.8% to RM2.7 million (FYE2015/16: RM1.6 million) on

the back of stronger contributions from Giesecke & Devrient

(Malaysia) Sdn Bhd.

CAPITAL EXPENDITURE (“CAPEX”)

During the year, the Group’s

CAPEX

decreased to RM14.0 million

compared to RM17.8 million in the previous year. The CAPEX

was incurred largely towards plantation development works, new

planting of oil palm and construction of worker’s quarters. Sources

of funds for CAPEX during the year were internally generated.

The cost of

Biological Assets

at financial year end decreased

by 33.4% to RM33.0 million compared to last year. This was

primarily due to RM24.8 million net impairment losses in PTNJL.

Additional CAPEX of RM8.7 million was incurred for plantation

development works and new planting programs at our estates in

Kelantan and Terengganu.

MANAGEMENT DISCUSSION AND ANALYSIS