31 / 174

31 / 174

performance

Annual Report 2017

29

On the back of lower FFB production, FFB processed reduced to

183,328 MT from 202,406 MT the previous year, a decrease of

9.4%. As a result, the cost of FFB increased by 39% to RM359.6

per MT, while the processing costs rose from RM27.2 per MT to

RM34.9 MT.

ESTATE DEVELOPMENT

During FYE2016/17, the Division spent RM12.1 million on CAPEX,

largely towards plantation development works and construction/

refurbishment of workers’ quarters.

PTNJL

As highlighted earlier by the Chairman in his Statement, PTNJL

is allowed to continue to operate its plantation operations until

the final determination of the status of its land by the Indonesian

2017

2016

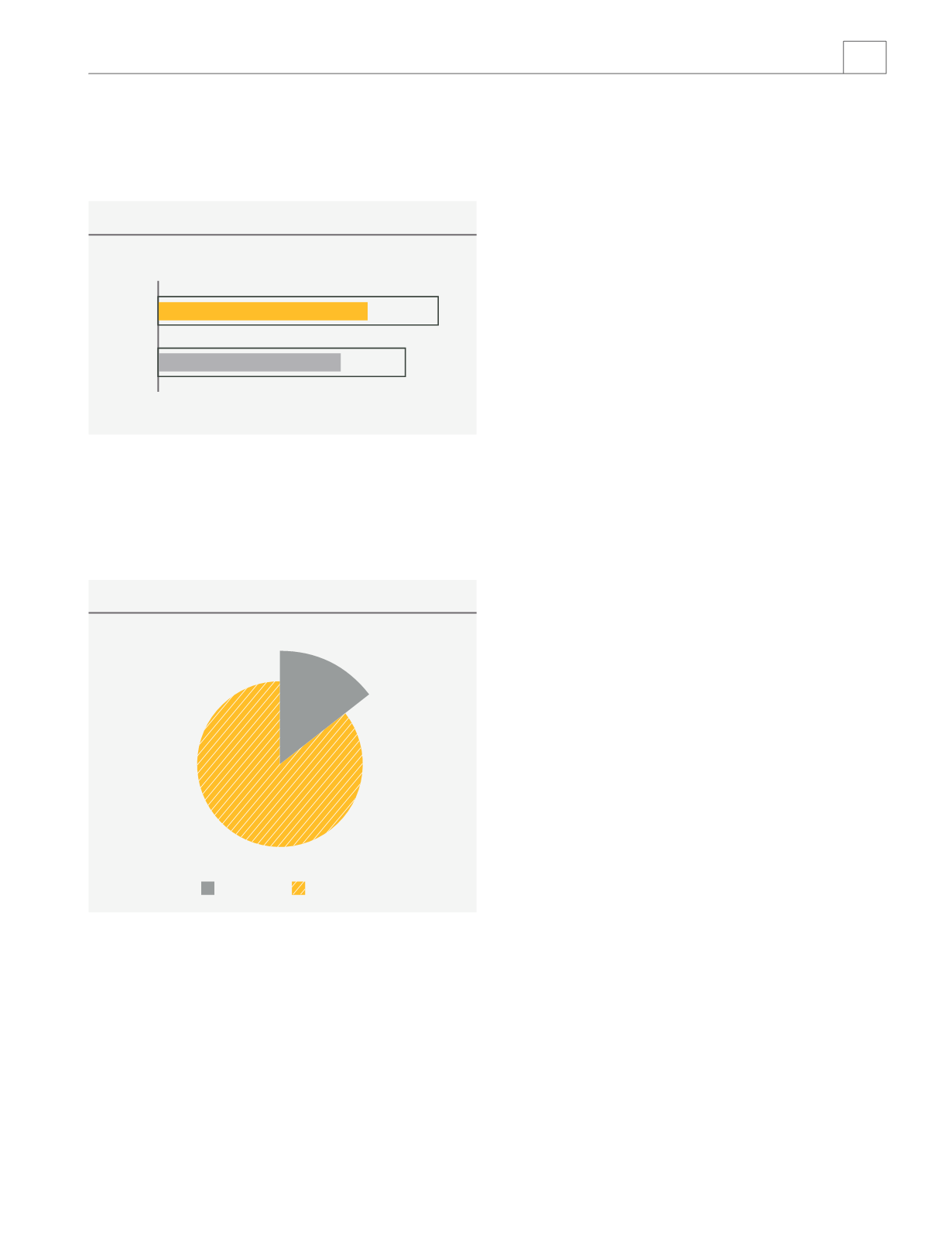

Oil Extraction Rate (OER %) Performance Y-o-Y

22.7

22.4

1,100.8

6,379.8

Planted Area (Ha)

Malaysia

Indonesia

courts. PTNJL’s planted area affected by the Ministerial Order

measures approximately 3,691.9 hectares. It is pleasing to

note that to-date, there has not been any disruption to PTNJL’s

operations and therefore there has not been any immediate

operational or financial impact on PTNJL.

Ladang Cendana, Kemaman, Terengganu

The planting program at Ladang Cendana has been completed,

and harvesting of the first planting had commenced in April 2017.

As at 31 March 2017, approximately 760.1 hectares have been

planted.

Ladang Dabong, Kuala Krai, Kelantan

A total of 110.0 hectares has been planted in FYE2016/17.

Planting on the remaining areas have been planned for this

current year.

Ladang Aring, Gua Musang, Kelantan

Progress continues on the new area with 230.7 hectares planted

during the year. Planting on the remaining areas has been planned

for this current financial year.

Ladang Sg Siput, Perak

The progress in obtaining the land development approvals have

been slow and are still pending to-date. Barring any further

delays, we expect to receive the said approvals by the end of this

current financial year

OUTLOOK

The commodity prices remain unpredictable on an expected

recovery in palm and soybean production, slow-down growth in

major markets like China as well as the effects of severe weather

patterns.

Nevertheless, and notwithstanding the final outcome of our appeal

and other actions available to us to annual the Ministerial Order,

the Board is of the view that this sector will continue to benefit

from the growing demand given that palm oil is a significant and

versatile raw material for both food and non-food industries, and

expect to see sustainable growth over the long-term.

In the medium term, we forecast an upward trend in FFB

production as more young areas in the Group’s greenfield estates

attain maturity and start to produce. Subject to palm-oil prices

remaining at healthy levels, growth in the Group’s FFB production

is expected to have a favourable impact on the Group’s revenue

in the coming years.

MANAGEMENT DISCUSSION AND ANALYSIS